If you are insuring your car in Perth, it is not just paperwork for your registration. It is the safety net that protects your income and your future car ownership when something goes wrong.

For many people in Western Australia, the car is more than transport. It is how you get to work, how you do rideshare, how you look after your family. If that car is off the road, your money stops, and your rent-to-own plan suddenly feels very stressful.

That is why understanding car insurance in WA matters, especially if you are new to Australia, on a visa, or moving from long-term rental to owning your own car.

Why Perth Drivers Feel Confused About Insurance

If you are a first-time car owner, rent-and-own customer, or rideshare driver, you might relate to this.

- You see “insurance included with rego” but do not know what it really covers.

- You hear words like CTP, third party, comprehensive, excess, and it all sounds the same.

- You search online, see many cheap options, and have no idea which one actually protects you.

- English is not your first language, and long policy wording feels stressful.

You are not alone. Many Perth drivers tick the box, pay the rego, and only find out what is not covered after a crash.

WA Rules You Must Know When Insuring Your Car in Perth

In Western Australia, there is a special system called Compulsory Third Party (CTP). This is linked to your vehicle registration. When you pay your rego, you automatically pay for CTP.

Important: CTP only covers injury to people if you cause an accident. It does not cover damage to your car. It does not pay for lost rideshare income. It does not protect your rent-to-own payments if the vehicle is written off.

This is where many first-time owners and rideshare drivers get caught. They think “rego includes insurance so I am covered”. In reality, CTP is only one small part of the story.

Why This Guide Is Different

If you are insuring your car in Perth, you need clear information, not insurance jargon.

This guide is written for:

- a first-time car owner in WA

- on a rent-to-own plan with no credit checks

- driving rideshare and relying on your car for income,

You will learn in simple language how CTP, third-party, and comprehensive insurance really work in Western Australia, what they do not cover, and how to choose protection that suits your situation today.

If you are still looking for ways to move from renting to owning, you may also find our guide to what rent-to-own actually means helpful as background.

Breaking Down Western Australia Car Insurance Types in Simple Language

In Western Australia, if you are insuring your car in Perth, there are three main types of cover you will hear about: CTP, third-party property, and comprehensive. Each one protects something different, and there are big gaps if you rely only on the basic level.

1. Compulsory Third Party (CTP) via WA registration

What it is

CTP is the insurance that comes with your WA vehicle registration. You cannot register a car without it.

What CTP covers

- Injury to other people if you cause a crash.

- Medical treatment and related costs for those injured people.

What CTP does not cover

- No cover for damage to your own car.

- No cover for damage to other people’s cars or property.

- No cover for lost income if you cannot drive for rideshare.

- No special protection just because you are on a rent-to-own plan.

CTP keeps you legal on the road, but it does not protect the car you are paying for, or the income you earn from it.

2. Third-Party Property Damage Insurance

What it is

This is an extra policy you buy from an insurer. It is not included in your rego. It is usually one of the cheaper options.

What third-party property covers

- Damage you cause to other people’s cars.

- Damage you cause to things like fences, walls, or buildings.

What third-party property does not cover

- No cover for repairs to your own car if you are at fault.

- No cover for your lost rideshare income while the car is off the road.

- Often, no coverage if you use the car for Uber or other rideshare, unless the policy clearly says so.

Third-party property coverage can help you avoid a very large bill for another driver, but when insuring your car in Perth, remember that your own vehicle may still be a total loss if you are at fault.

3. Comprehensive Car Insurance

What it is

Comprehensive is the widest level of cover for the car itself. It usually costs more each week, but it can save you a lot if something serious happens.

What comprehensive insurance often covers

- Damage to your own car if you are at fault.

- Damage to other vehicles and property.

- Theft, fire, and sometimes weather damage.

Important gaps and differences

- Not all comprehensive policies allow rideshare use. Many only cover “private use”, so Uber work can void your cover.

- Excess amounts can be high, especially for younger drivers or visa holders.

- Downtime cover, which helps if your car is off the road, is not standard. You often need specialised rideshare-focused coverage for this.

Two policies can both be called “comprehensive,” but they offer very different levels of protection and costs. When insuring your car in Perth, you need to carefully read the sections on rideshare use, excess, and exclusions before making a decision. If you are using a hybrid for full-time driving, it can be worth matching your cover to a clear plan, similar to how you would compare ongoing fuel and operating costs using a guide like the weekly cost of running a hybrid for Perth drivers.

Insurance for Rideshare Drivers in Perth: What You Need to Know

If you drive Uber or another rideshare in Perth, insuring your car is different from that of a normal private driver. You are using your car to earn money. That changes the risk and what your policy must allow.

Why Standard Car Insurance Often Does Not Cover Rideshare

Most basic policies are written for “private use”. That usually means:

- Driving to work and home

- Personal trips and family use

- Not using the car as a business tool

Once you switch the app on and start taking paid trips, you are using the car for commercial work. If your policy does not clearly allow rideshare, the insurer can say no when you claim.

Key warning sign: When insuring your car in Perth, if the policy only mentions “private use” or is silent about Uber or rideshare, it probably does not cover your work trips.

Why Do You Need A Rideshare-Approved Comprehensive Cover

For most Perth rideshare drivers, especially if you are on a visa or rent-to-own plan, rideshare-friendly comprehensive cover is the safer option because it can:

- Cover damage to your own car

- Cover damage to other cars and property

- Apply while you are logged in to the app, carrying passengers, or on the way to a job (if the policy is written for rideshare)

If your car is part of a rent-to-own setup, properly insuring it in Perth is important. Losing the vehicle without the right cover can leave you with unpaid costs. You can learn more about how this works if a vehicle is written off by reading guides such as ‘What happens when a lease car is written off?’

Excess, Downtime, And Claim Limits

Excess is the amount you pay from your own pocket when you make a claim. For younger drivers and some visa holders, insurers often add extra excess amounts. This means:

- Your base excess might be one figure

- Plus a “young driver” excess

- Plus, sometimes an extra amount for rideshare use

So a small crash can still cost you a large out-of-pocket bill before the insurer pays anything. When insuring your car in Perth, if you are under 25, always check the “young driver excess” section and any extra charges for rideshare use.

Downtime is the period when your car is off the road after an accident. During this time:

- You might have no rideshare income

- You might still need to pay rent, to own weekly fees, or other bills

Standard policies often do not pay you anything for lost income. Some rideshare-focused covers include a daily or weekly benefit, but this is not automatic. You need to read the section on hire car, income cover, or downtime.

Claim limits are the maximum the insurer will pay in different situations. Look for limits on:

- Total payout if the car is written off

- Towing, storage, and hire car costs

- Any special rideshare-related benefits

How to Avoid Claim Rejections as A Rideshare Driver

When insuring your car in Perth, and to keep yourself legal and protected while driving Uber or other rideshare in Western Australia, use this simple approach:

- Tell the insurer you are a rideshare driver. Do this at the start, not after an accident.

- Check the “use of vehicle” section. It should clearly mention rideshare or similar words, not just “private use”.

- Ask about excess for under-25s and visa holders. Get the amounts in writing so there are no surprises.

- Look for downtime or income protection. If your car is your main income, this point matters.

- Match your cover to how you drive. If you are driving full-time and planning to own the car long-term, you may find resources like renting vs owning a car for rideshare drivers useful for the bigger picture.

If you keep your CTP current through WA registration, have rideshare-approved comprehensive cover, and understand your excess and limits, you are in a much stronger position whenever something goes wrong on the road.

Common Mistakes People Make When Insuring Their Car in WA

Many Perth drivers only discover their insurance mistakes after a crash or a claim. When insuring your car in Perth, small misunderstandings can turn into expensive problems. At that point, it is too late. Repair costs and lost income are already sitting in front of you.

Mistake 1: Confusing CTP with Wull Insurance

This is one of the biggest problems for new migrants, first-time homebuyers, and rent-to-own drivers.

- They see CTP included with WA registration and think “my insurance is done”.

- They assume CTP covers damage to their own car and other cars.

CTP only covers injuries to people. If you have no extra cover and you hit another car, you could be fully responsible for all repair costs, and your own car will be your problem too.

Mistake 2: Ignoring how Excess Really Works

When insuring your car in Perth, many drivers focus only on the weekly or monthly price and skip the excess section.

- They do not realise there can be a base excess plus an extra excess for young drivers.

- Some policies also add extra excess for rideshare use or certain locations and times.

The result is a nasty surprise at claim time. You might think you will pay one amount, but the real excess is several times higher. For rent-to-own customers, this can break the budget and risk missed payments.

Mistake 3: Assuming Every Policy Covers Rideshare

Many comprehensive policies in Western Australia are written for private use only.

- They might stay silent on Uber or rideshare.

- They might list “business use” conditions you do not meet.

If you have an accident while the app is on and your policy does not clearly cover rideshare, the insurer can refuse the claim. When insuring your car in Perth, you must confirm rideshare use is allowed. Otherwise, your car can be off the road, your rideshare income gone, and you might still owe money on a rent-to-own plan.

Mistake 4: Forgetting About Downtime Risk

Most people focus on “Am I covered for repairs” and forget to ask “What happens to my income while the car is in the workshop”.

- No income from Uber or delivery work.

- Ongoing weekly rent, then own payments.

- Extra travel costs to get to another job or study.

Standard policies often pay nothing for this lost time. When insuring your car in Perth, check whether the policy includes hire car or income-style benefits before you buy. Some rideshare-focused covers include these, but many do not. If your whole plan is to move from renting to owning, it helps to think about protection the same way you think about long-term costs when comparing rent-to-own options with normal car finance.

Mistake 5: Choosing the Lowest Price Without Reading Details

It is easy to jump on the lowest quote, especially if money is tight or you have had credit problems before.

- Cheap policies can have high excess.

- They might not allow rideshare use.

- They can have low payout limits and many exclusions.

Low weekly cost can still mean high risk.

For first-time buyers and rent-to-own customers in Perth, the smarter move when insuring your car in Perth is to balance price with cover. Check what is included, what is excluded, and how it fits with the way you actually drive and earn in Western Australia. If your car is a hybrid that you plan to keep long term, you might also want to think about how your insurance choices fit with your bigger ownership plan, the same way you would when looking at guides like the benefits of owning a hybrid for regular and rideshare driving.

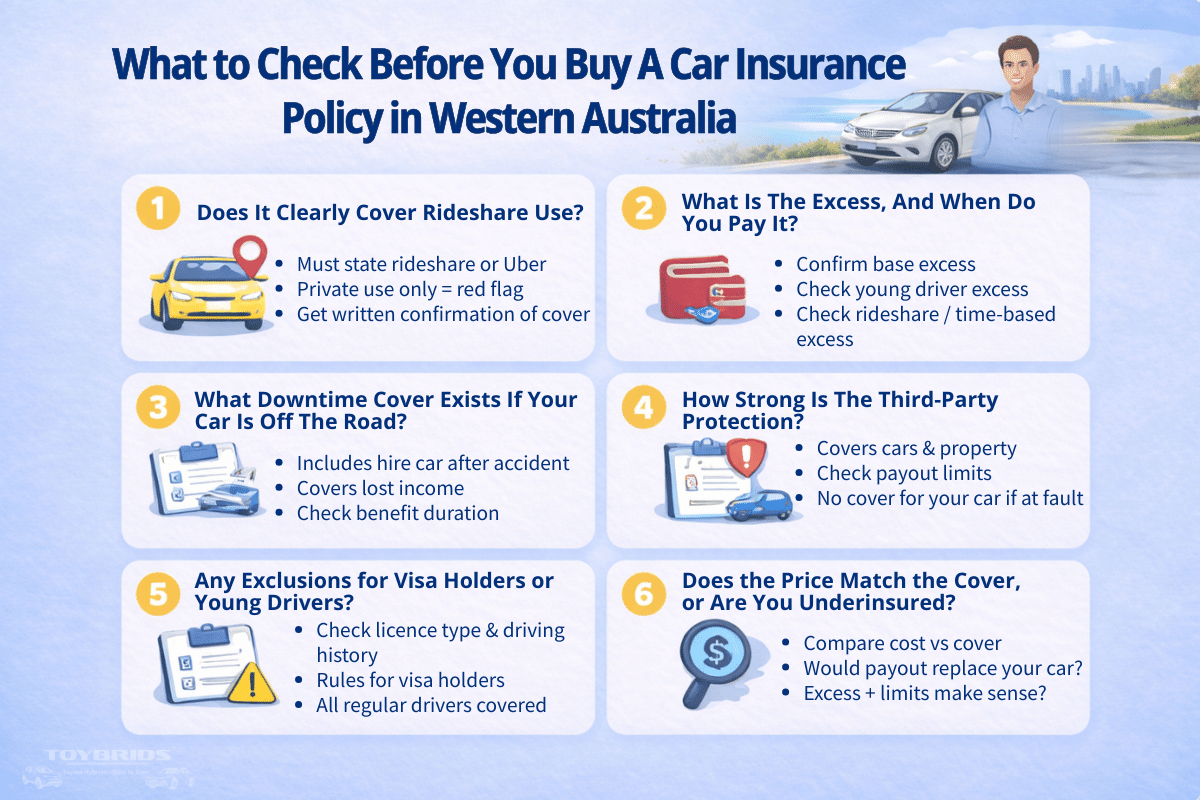

What to Check Before You Buy A Car Insurance Policy in Western Australia

Before you say yes to any policy in WA, use this simple checklist. It helps you avoid hidden gaps that can hurt your wallet, your rent-to-own plan, and your rideshare income.

1. Does It Clearly Cover Rideshare Use?

- Look for clear words like “rideshare” or “Uber” in the use of vehicle section.

- If it only says “private use”, that is a red flag.

- Ask the insurer in plain language, “Am I covered while I am doing rideshare trips?” and get the answer in writing.

If you drive for income, do not guess. Make sure rideshare is allowed.

2. What Is The Excess, And When Do You Pay It?

- Find the base excess amount.

- Check for extra excess for younger drivers.

- Check for extra excess for rideshare use or certain times of day.

Use a simple test when insuring your car in Perth. Ask yourself, “If I had a small crash tomorrow, could I really afford this total excess from my savings or next few pay cycles?”. If the answer is no, that policy may be risky for you.

3. What Downtime Cover Exists If Your Car Is Off The Road?

- Check if the policy includes a hire car after an accident.

- See if there is any benefit that helps with lost income.

- Confirm how long any hire car or benefit lasts.

If your car is your main income or your way to get to work, downtime matters as much as repair costs.

4. How Strong Is The Third-Party Protection?

- Make sure the policy covers damage to other cars and property, not just injuries.

- Look at any payout limits for third-party damage.

- If it is only basic third-party property, remember your own car is not protected if you are at fault.

If you are moving from renting to a rent-then-own setup, it helps to think long term when insuring your car in Perth. Some drivers like to match their cover to the kind of car they plan to keep, for example, a reliable hybrid that suits both personal and rideshare use. For more on that, you can read guides like comparing hybrid and electric options for Perth drivers.

5. Any Exclusions for Visa Holders or Young Drivers?

- Look for sections about driver licence type, years of driving, or visa status.

- Check if the policy has stricter rules for temporary visa holders.

- Confirm that all regular drivers on your car are allowed under the policy.

If you are on a student, graduate, partner, or temporary visa, do not skip this part. Some policies look cheap but quietly exclude your situation.

6. Does the Price Match the Cover, or Are You Underinsured?

- Compare the weekly or monthly cost with what the policy actually covers.

- Ask yourself, “If the car was a total loss, would this payout get me back on the road?”.

- Check that the excess plus any payout limit makes sense for the real value of your car.

Cheap premium with weak cover is not a bargain.

If you are using a rent-to-own plan with no credit checks, the goal is simple: get the car. If you want an independent government overview of your insurance rights and policy options, you can review the consumer guide at Moneysmart.gov.au. When insuring your car in Perth, protect the vehicle you are working hard to own and the income that pays for it.

Practical Advice to Make Smart Car Insurance Choices in Perth

Here is a clear way to think about car insurance if you live and drive in Perth right now. Whether you are a first-time owner, a rent-and-own customer, or a rideshare driver, these steps will help you stay protected without wasting money.

1. Keep Your WA Rego and CTP Up to Date

- Make sure your vehicle registration in Western Australia is always up to date.

- Remember, CTP comes with your rego and covers injury to people, not damage to cars.

- Set reminders for when your rego is due so you never drive an unregistered vehicle.

CTP keeps you legal, but it is only the first layer of protection.

2. Protect Your Income and Your Ownership, Not Just Your Plate Number

- Ask yourself, “If my car were written off tomorrow, what happens to my job or rideshare income?” When insuring your car in Perth, think beyond the legal minimum.

- If you are on a rent-to-own plan, think about what happens to your payments if the car is a total loss.

- Choose a cover that helps you get back on the road, not just a cover that ticks a legal box.

If you are still learning how rent-to-own works, you can read more in guides like Can You Rent to Own a Car in Perth.

3. Do Not Chase the Cheapest Quote; Look for the Best Value

- Compare the excess, exclusions, and payout limits, not just the weekly price.

- Be careful with “budget” policies that look good now but leave big gaps later.

- Pay a little more if it means a fair excess and proper rideshare cover.

Cheap premiums with poor cover can cost you more when something goes wrong.

4. Use Rideshare-Specific Cover If You Drive Uber or Similar

- Tell the insurer clearly that you use the car for rideshare in Perth.

- Make sure the policy says it covers rideshare use, not just “private use”.

- Check how your cover works when the app is on, when you are on the way to pick up, and when a passenger is in the car.

If your whole plan is to run a fuel-efficient car for private and rideshare use, it helps to understand how your hybrid works when insuring your car in Perth. You can learn more by reading guides like “How Toyota hybrid systems work for Perth drivers.”

5. Review Your Policy When Your Situation Changes

- If you start or stop doing rideshare, update your cover.

- If you move from renting a car to a rental, then own a plan, check the insured value and excess.

- If you change jobs, move to a different suburb, or add a new driver, let the insurer know.

Your insurance should reflect your real-life driving in Perth, not how you were driving [insert time period] ago.

You are allowed to ask questions, and you should.

When insuring your car in Perth, keep your WA rego and CTP current, choose cover that protects your income and ownership, avoid cheap policies with nasty surprises, use rideshare-ready cover for Uber work, and review your policy as your life changes.

You then put yourself in a much safer position on Perth roads. You can drive, earn, and move toward owning your car with more confidence and less stress.

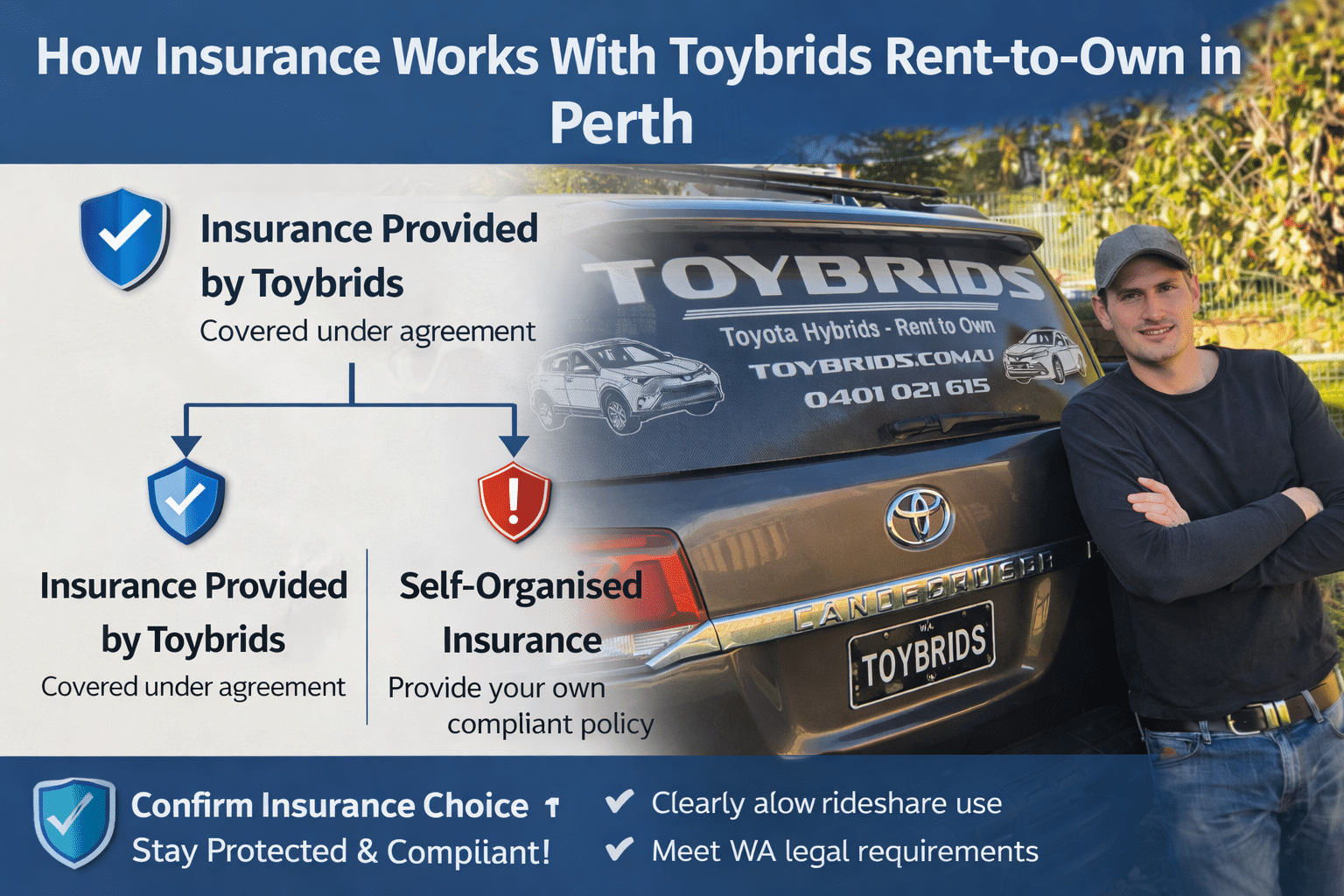

How Insurance Works With Toybrids Rent-to-Own in Perth

If you choose a Toybrids rent-to-own vehicle, insurance can be included in your agreement. This removes the stress of finding a separate policy while you are insuring your car in Perth and starting rideshare work.

Some drivers prefer to organise their own cover because they have found a better deal or want to manage it themselves. That is allowed. However, this decision is formally recorded in the contract, confirming that you chose to reject the included insurance and take full responsibility for arranging your own compliant cover.

This protects both you and the other driver when insuring your car in Perth.

If you organise your own policy, it must:

- Clearly allow rideshare use

- Meet WA legal requirements

- Remain active for the full term of your agreement

The goal is simple. Protect the car. Protect your income. Stay compliant on Perth roads.